Q3 Performance Update

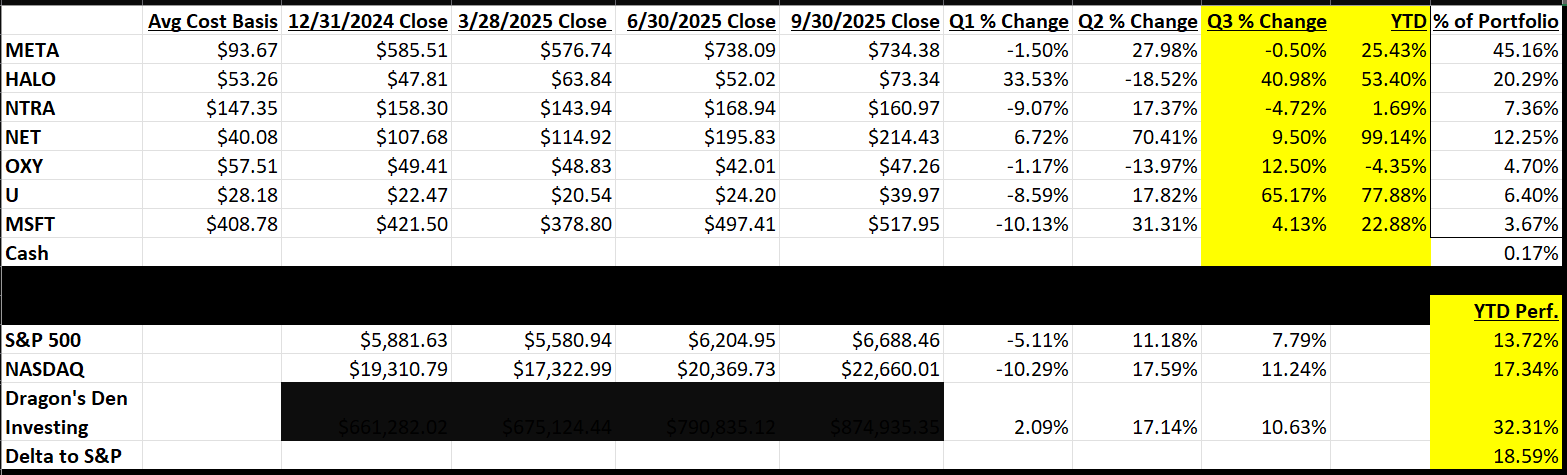

The period of July, August, and September was smooth sailing for stocks. The S&P was up 7.8% while the Nasdaq leapt even higher at 11.2%. My portfolio mostly tracked market performance at 10.6% in Q3. What I found surprising was how semiconductors roared back, particularly in September, which was the primary reason for the strong market performance. Stocks like Nvidia, Micron, and (gasp) Intel are up huge just in the past month sparking talk of an AI bubble. It does seem like the picks and shovels of AI trade should be priced in by now, but the market is showing strength because everywhere else to put money is undesirable.

I normally compare myself to the S&P 500 because if I wasn’t actively picking stocks I would be working full-time and plowing all of my free cash into the index. I’ve begun to re-think this and come to the conclusion that my “performance” actually should be the difference between the index and my portfolio. So for example if I would have made $100K in the market index and I made $250K from active management, then my time yielded $150K not $250K. This should also be the benchmark for years when the market is down.

As of Q3 close I am YTD up 32.3% while the S&P 500 was 13.7%, a difference of 18.6%. It’s always nice to see yourself doing as well or better than the hedge funds, which many retail investors seem to be doing this year. It’s also interesting how few actually outperform the index by any significant margin.

Below you can see how my stocks and portfolio break down by quarter:

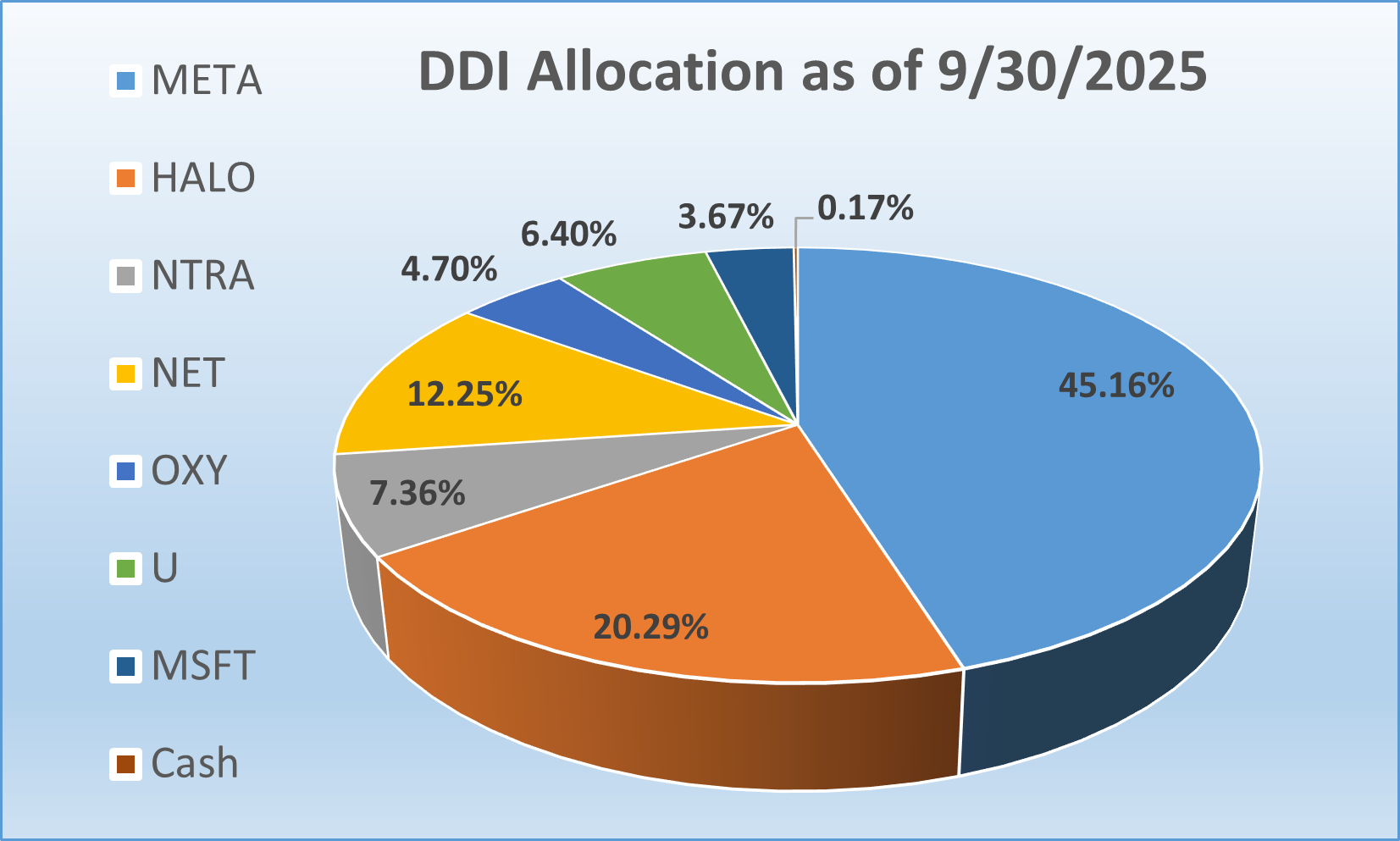

My current portfolio has re-balanced itself somewhat to be more heavily weighted to the stocks which have performed well this year — namely NET 0.00%↑ and HALO 0.00%↑.

Looking Ahead:

The first few days of October were rough on my main positions, but I think this is based on mostly short-term concerns. Every single one of my stocks has been driven by earnings momentum rather than sentiment, so the next month should be positive. A few thoughts on each position (listed by portfolio weight), then full dollar transparency for paid subscribers:

META: What became clear in Q3 is that Meta is very much lagging OpenAI and Google in AI. Couple this with Zuckerberg’s open ended commitments to spend $600B on data centers, and some are thinking perhaps the company will go down the road of over-investment into something that will not yield results like the Metaverse. I think the stock could see some more near-term pressure, but I’d rather own a stock over-investing in the future than one under-investing in it (e.g. Apple). If Zuckerberg can control himself on the earnings call then the earnings numbers should still hold the stock price high.

HALO: I am a big fan of this stock and still think it has some running room even this year. They made a sizeable acquisition this past week which I think compliments their core positions. As I said in my original thesis, I think this is the company to own if you believe injectable medicines will become more prevalent, and their willingness to acquire competitors shows this has been correct. I am very happy as an investor to see them double down on their core competency rather than investing in a different area they don’t understand in order to diversify.

NET: I wrote in February why I think Cloudflare is a great stock, and it’s up 99% YTD. The question now really is with such a premium valuation, does the stock still warrant holding? For me it is as I follow the company closely and see the pace and amount of innovation that comes from the company on a weekly basis. Cloudflare is very well situated for the post-search web, and their culture+execution is incredible. Whenever I read about a new product they’ve just released I often think to myself “I don’t own enough of this stock.”

NTRA: This stock has gone nowhere in 2025, but that’s mostly because it had such a standout year last year and much of its potential is priced in. They need to continue to execute well on earnings, and so far in 2025 they have. I think it is only a matter of time before the stock starts running again as it did last year. AI utilization in the medical field is just getting warmed up.

U: I wrote about Unity last week and since that article was published the stock has gone down 12%. It’s always interesting to see that when new AI model features come out (in this case OpenAI’s Sora), Unity tends to go down. I find this odd because my entire thesis relies on there being more content that is more easily produced as a catalyst for Unity’s software which will stitch together this content into actual products. I think it’s a good thing to have a thesis for a stock that is counter to market action if you are going to hold for the long-term.

OXY: Still considering selling this one even though oil should rise as Trump puts pressure on Putin and the war escalates. There always seems to be some kind of catalyst in my mind for why oil should go up, then it rarely ever does. That is a sign that I should sell.

MSFT: Still my favorite Mag7 position outside Meta. Not much else to say here, other than that my previously published thoughts from 2024 still hold.