Why I Got Nvidia Wrong

There is no subject which has occupied my mind more in relation to the stock market this year than that of Nvidia and why I didn’t invest in it early. Surely every investor who doesn’t have money in Nvidia is kicking themselves, and everyone who does own the stock feels like a market savant. The question is especially painful for me because I had a job offer from Nvidia in 2017, and at that time even told family to put money into the stock when the price was ~$30. Rather than join Nvidia, I decided to accept an offer from Intel because the base salary was significantly higher. As can be viewed below, even a modest yearly stock based compensation of $30,000 would have grown to around $1M today. For Intel, it shrinks to about $20,000.

Yet mistakes related to Nvidia do not end there, as this past year I wrote the following in 2024 Market Outlook and Framing:

Tech Trends - Market Movers in 2024

AI Cost and Monetisation Effects:

I expect AI to dominate tech in 2024 - it is not a fad like NFTs/cryptocurrency, but something that will fundamentally change the way humans live in the future. AI will slowly proliferate into every product and human experience one can possibly think of; but what remains to be understood is which companies will figure out how to monetise AI in a way that exceeds the immense cost of both training the necessary algorithms and actively running the use cases themselves (e.g. ChatGPT costs x cents every time someone makes a query, so it’s not designed for scaling and monetisation in its current form).Until monetisation become clearer, the safest AI play for stocks is in the semiconductor sector, where I own both AMD and INTC. NVDA is seen by most as the assured AI play, and accordingly it is up 240% over the past year. I think Nvidia is somewhat over-hyped in comparison to my holdings, and so having missed the initial run-up in Nvidia’s stock, I still favour holding alternatives such as AMD and INTC while NVDA margins and stock price remain so high.

Rarely can a statement be both so right and so wrong all at once. The trend predicted turned out to be correct, yet in 2024 Nvidia is currently up 128% YTD, while AMD is up 21% and Intel is down 35%.

Rather than feeling sorry for myself, this painful experience should be viewed through the lens of learning. In this week’s article we will examine why I got Nvidia wrong.

Nvidia and Pricing Power:

"The single-most important decision in evaluating a business is pricing power. If you've got the power to raise prices without losing business to a competitor, you've got a very good business. And if you have to have a prayer session before raising the price by a tenth of a cent, then you've got a terrible business.”

— Warren Buffett

While I worked at Intel there was always a great deal of fear around raising prices, yet across the street at Nvidia they would raise prices with reckless abandon whenever the opportunity presented itself (gaming products during COVID, cryptocurrency mining, etc). This was not because Intel executives were timid or stupid, but rather because they knew the market would not sustain price increases on a product that was not desired in the way Nvidia’s had come to be during those times.

The same phenomenon exists today in the AI boom, but on steroids. In the data center space, Nvidia has been able to raise prices and expand margins massively — without losing share to AMD or other competitors. Nvidia did the same thing with personal computing GPUs previously, so why did I think it would be any different in the data center? Three primary reasons, all of which were a misread of the situation.

Economic Factors —

The ZIRP (zero interest rate policy) era of “cheap” money was over, and thus public corporations became far more careful on spending. This led to many companies announcing large layoffs and rolling out years of efficiency. In such an environment, would these same companies be willing to massively increase their capital spend and stomach price increases while doing so? My view was that they would be hesitant to, and therefore AMD (a far less pricey alternative) would benefit. In actuality, Nvidia’s product performance and software moat were so strong that their customers (e.g. Meta, Microsoft, etc.) thought they would lose to competitors if they did not buy Nvidia. Therefore, in the continuing AI gold rush of 2024, the only game in town turned out to be Nvidia. Nvidia’s customers have been willing to pay anything for their GPUs, leading Jensen Huang to remark that Nvidia’s GPUs are “so good that even when the competitor's chips are free, it's not cheap enough.”This may slowly be starting to change (see below from Microsoft on May 17), but Nvidia or bust has been the reality for the last 1.5 years of the initial AI boom, and I misread it.

Microsoft recently announced they would be offering AMD chips in Azure as an alternative to Nvidia for AI workloads. In addition to the end of ZIRP, the Biden administration FTC has essentially removed any incentive for large tech companies to utilize capital for M&A (mergers and acquisitions). I did not realize the extent of this, but it has been important for shifting the cash of the largest tech firms towards inward investment such as infrastructure (GPUs), share buybacks, and dividends (Meta and Google announced dividends for the first time ever).

Customer Negotiating Power —

In the client space, most of Nvidia’s customers are relatively small companies (think ASUS, Dell, MSI, Zotac, etc). These companies have little to no negotiating power to push back against Nvidia price increases. They know that if their products do not have Nvidia inside, then their finished products (such as PCs) will lose to competitors that do, so they stomach any price increase. For the likes of Meta, Microsoft, Amazon, and others, I assumed they have more negotiating power to push back against large price increases for data center GPUs. Yet because they do not want to lose to their own competition, these cloud giants have thrown every cent of capital to acquire as many Nvidia GPUs as possible, leaving little money left for AMD and other alternatives. In a supply constrained environment, the game is to see who can get the best GPUs at any cost, because there are only so many of them and whoever doesn’t get them will theoretically fall behind. Negotiating power turned out to be of little consequence, other than to show that all power lies with the market leader in a boom.Supply Constraints —

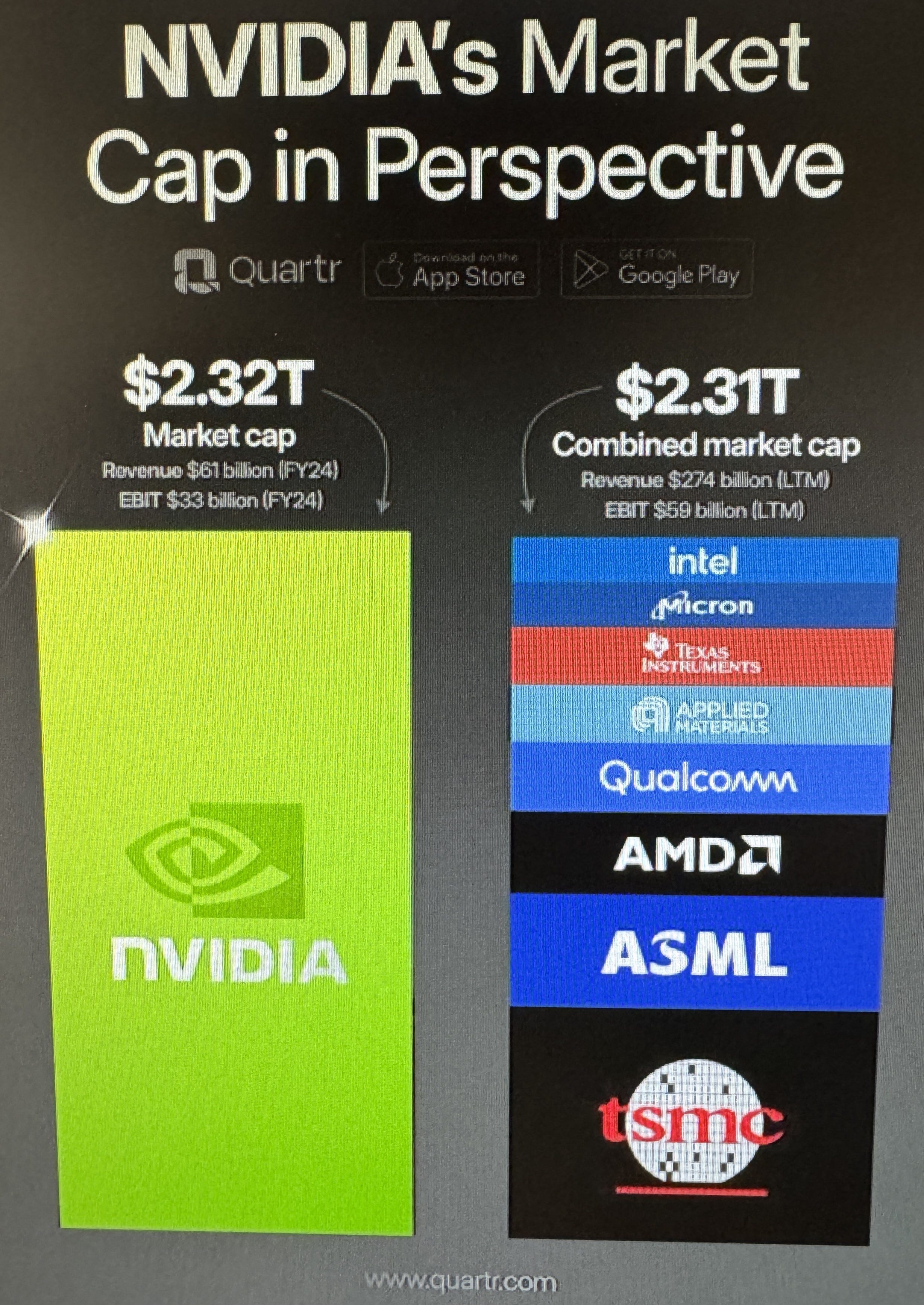

Nvidia and AMD currently have one source for their data center GPUs, and that’s TSMC in Taiwan. Generally in times when demand outstrips supply, orders are booked out for years. One could then assume that because Nvidia could not radically increase supply in this environment, that their upside would be limited at least in the amount of chips they could potentially sell. This again was wrong, as Jensen Huang made multiple trips to Taiwan courting TSMC’s top executives for additional supply, and apparently was able to secure it (every quarter they beat and raise).Nvidia’s pricing power gives them the ability to take any supply that becomes available (or perhaps even take it from others). For instance, if Nvidia can charge the likes of Meta $40,000/chip, but AMD is only able to charge $20,000, who should we assume TSMC is making more money from? In a normal environment, the answer should be that the prices are similar, yet today we can bet that any supply that opens up is secured by Nvidia because they can pay more for it and still make more money per chip than their competition — so of course Nvidia wins any additional supply as TSMC also benefits from the situation. This is apparent in TSMC’s strong earnings throughout 2024 (TSMC is up ~49% YTD).

Additionally, I made the incorrect assumption that wall street would see a semiconductor space that is supply constrained on the manufacturing side, and give a nod of confidence to Intel and Pat Gelsinger’s IDM 2.0 strategy, which will drastically increase leading edge supply for AI chips in the future. Intel has made a series of blunders in 2024, and has lost market share in the data center as Nvidia vacuums up every cent of server capital. It should have been obvious that Intel was more of a 2025-2026 play, and that this year my investment in Intel could have been shifted to Nvidia, and then shifted back to Intel at the start of 2025.

Relative Market Capitalisation:

During most of my career in the semiconductor space, Intel was the largest company by market capitalisation at around $250 billion. Slowly Nvidia and AMD began to eclipse Intel, but it was inconceivable to myself and many others that a semiconductor company that focuses on designing hardware could sustain valuation at more than $1 trillion. This experience shows the bias of being in an industry, and how that can creep into investment decisions. As a result, each valuation milestone Nvidia surpassed was perceived as now the stock is “too expensive.” The assumption being that the stock would correct at some point, giving myself and other investors an opportunity to enter at a lower price — of course it never did and is now worth $2.7T.

One mental exercise I’ve used when evaluating stocks is to look at the market cap of a company compared to its peers. Then based on technology trends, ask myself questions such as, which of these companies is more likely to double in valuation over the next year or two? At the end of 2023, Nvidia was worth $1.1T and AMD was worth $250B. If both stood to benefit from the AI boom (as I believed), would it be more likely that at the end of the year Nvidia would be worth $2.2T or that AMD would be worth $500B? The lift for AMD to add $250B of market cap should have been easier considering no semiconductor company had ever even been worth $1T, let alone added that much valuation in a single year — yet Nvidia did it in less than 6 months.

Holding Bias and Missing the Train:

Over the past year I’ve read and listened to an immense amount of Charlie Munger. For the most part, this has been enlightening, but it has also resulted in an unhealthy aspiration to emulate Charlie’s “sit on your ass investing methods.” Even when I near a conclusion that a previous decision was incorrect, I feel a pull towards seeing the thesis through to its conclusion. While I have no plans to become a day trader, I have begun to think that there may be a happy medium as I am not (nor is practically anyone), an intellectual peer with Charlie Munger.

This isn’t to say I haven’t benefited greatly from sitting on my ass in current positions. I bought AMD at $19 in 2019, and now it is at $167. I bought Meta at $93 and now it is at $467. Yet these gains pale in comparison to what a similar position bought in 2019 Nvidia would have yielded.

For investors such as myself who like to buy low rather than when a stock is already rising rapidly, Nvidia has been one many have missed out on. This has also been a great learning experience, and something I will sparingly and begrudgingly change for the future — even if I don’t buy at the bottom, a stock may still be well worth buying. Buying high can still be worthwhile, as long as the thesis is extremely robust (e.g. Nvidia at end of 2023).

So You’ve Made Mistakes — Now What?

I hesitate to predict what will happen next with Nvidia. I do not see its business cratering in the near-term, but given that its valuation is already nearing $3T I cannot recommend investing now. In February we wrote that Nvidia could become the most valuable company in the world sometime this year, but would eventually come down after a semiconductor demand cycle took place. I should have put money in that very day, and sold later this month. Absent a time machine, our position since February has not changed. There are those who believe that Nvidia will reach $10T by 2030, and it may seem crazy to consider. Yet just a couple years ago most would have thought it equally crazy to think Nvidia would be worth $3T in 2024.

I’m still holding out for the cyclical nature of the semiconductor industry before re-evaluating putting money into Nvidia, as the stock price again looks too high today. Additionally, I still think AMD will have a strong 2H 2024. So perhaps one could conclude that I haven’t learned anything at all.